European EV Market Shows Positive Momentum in January 2025

The European passenger plugin vehicle market kicked off 2025 with a strong performance, registering 244,000 vehicles in January, representing an 18% year-over-year (YoY) increase. Battery electric vehicles (BEVs) led the charge, with 168,000 units sold, a 37% rise compared to the previous year. This growth occurred despite reduced EV incentives in certain markets. Plugin hybrids (PHEVs), however, experienced a 5% YoY decline, totaling approximately 76,000 units.

BEVs held a significant market share advantage over PHEVs at the start of the year, accounting for 69% of plugin sales compared to PHEVs’ 31%. This is a notable shift from the previous year, when BEVs held a 61% share and PHEVs 39%.

Despite an overall market slowdown of 3% YoY to just over one million units, the BEV share reached a robust 17% in January 2025 – a considerable increase from 12% in January 2024 and 10% in January 2023. Concurrently, plugless hybrids continued their upward trajectory, increasing from a 26% share in January 2023 to 29% in January 2024, and reaching 35% currently. Petrol vehicle sales decreased by 21% YoY to 29% share, while diesel further declined, falling from 16% in January 2023 to 12% a year ago, and now at just 9%.

At the current rate, diesel new car sales are projected to diminish by 2028. This also means that 59% of all passenger vehicles sold in Europe were electrified. If this pace continues, all new car sales in Europe, in some form, are expected to be electrified by 2030.

With a BEV share of 17% at the start of the year, the plugin market is projected to grow throughout the year and approach a 30% plugin share by the end of the year. BEVs are predicted to account for two-thirds of that, or around a 20% share of the overall auto market. This represents a shift from the 23% plugin vehicle share in 2024, the 24% in 2023, and the 23% in 2022.

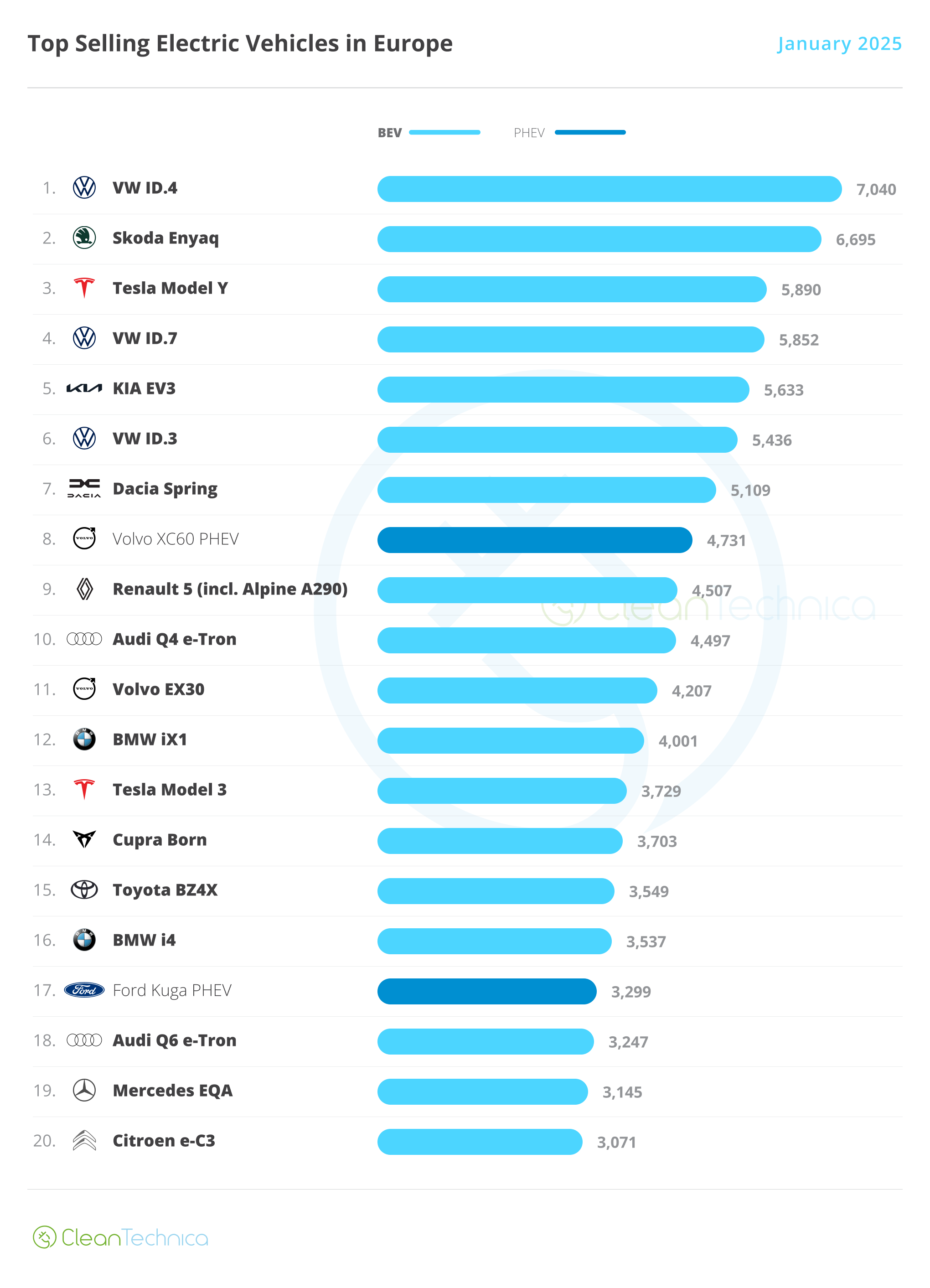

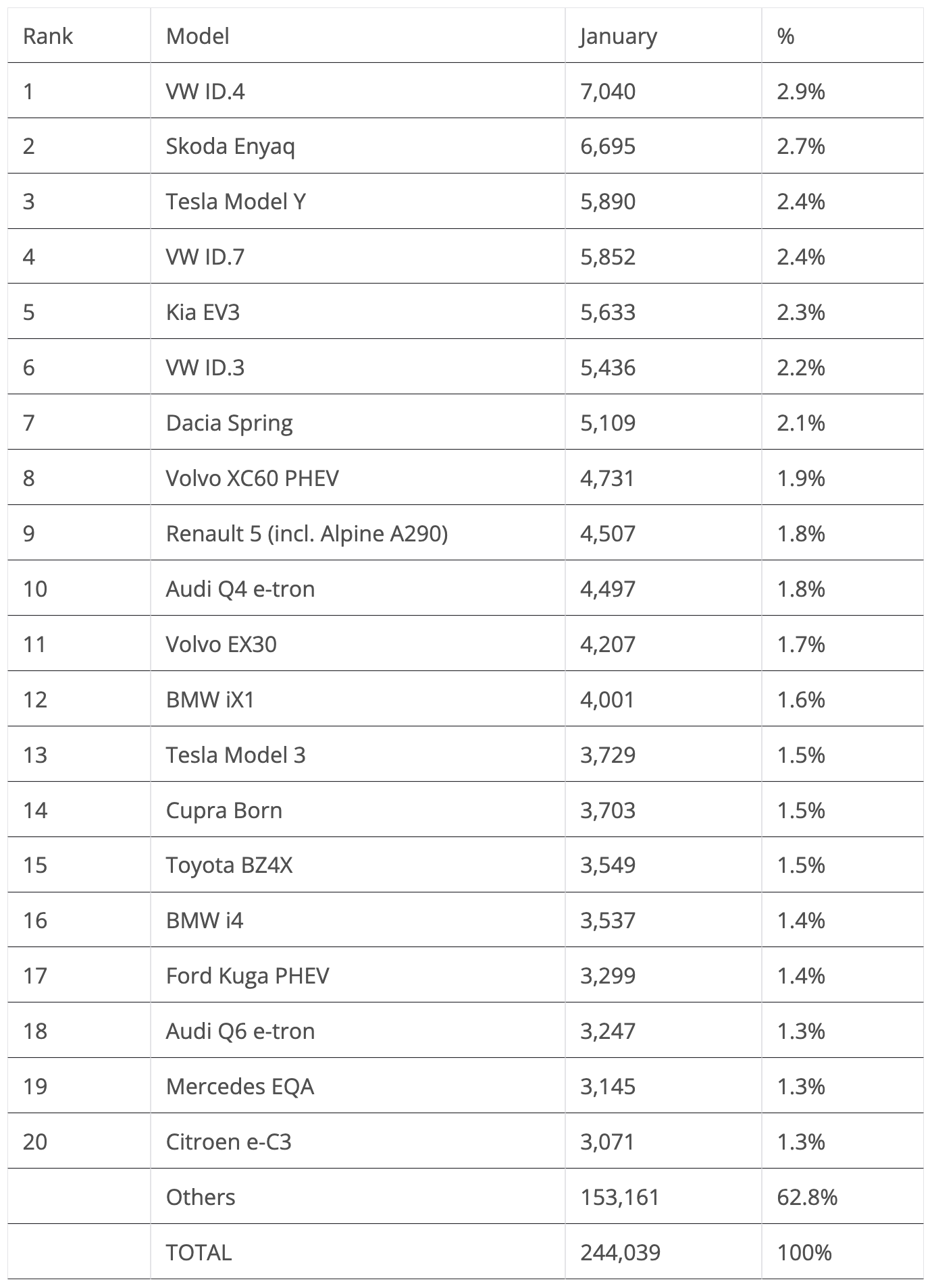

Model Rankings: Surprises and Familiar Faces

January’s sales saw Volkswagen take an early lead, while Tesla and other manufacturers were still recovering from their end-of-year peaks that led to some exciting shifts at the top of the rankings, with three of the top five models hailing from the Volkswagen Group.

The top five models for January are:

- VW ID.4: The German crossover achieved its first monthly win in years with 7,040 registrations. Though this lead may be short-lived, a podium finish in 2025 is seen as likely, perhaps the ID.4 could even surpass the Model 3 for second place, improving on its bronze medals from 2022 and 2023.

- Skoda Enyaq: The 6,695 deliveries in January placed the Enyaq in second place. The expected launch of Skoda’s new Elroq model could impact the Enyaq’s position as the Elroq ramps up production.

- Tesla Model Y: The made-in-Germany crossover secured third place, with 5,890 registrations, a 49% decrease compared to January 2024. Although sales dipped, the upcoming refreshed version is expected to boost sales. Tesla hopes to maintain its two models in the top positions by the end of the year.

- VW ID.7: The German liftback recorded 5,852 registrations, hitting its second consecutive record month. This increase in popularity is attributed to the introduction of the station wagon design and the GTX version.

- Kia EV3: Kia is ramping up sales of its newest model, with 5,663 registrations last month. The EV3 is poised to follow in the successful steps of the Kia Niro. The next couple of months will show if the EV3 is a podium contender or if a top 5 presence is already its peak.

Outside of the top 5, the Dacia Spring, Toyota BZ4X, Renault 5, Citroen e-C3 and Audi Q6 e-tron also deserve mentions for their performances this month.

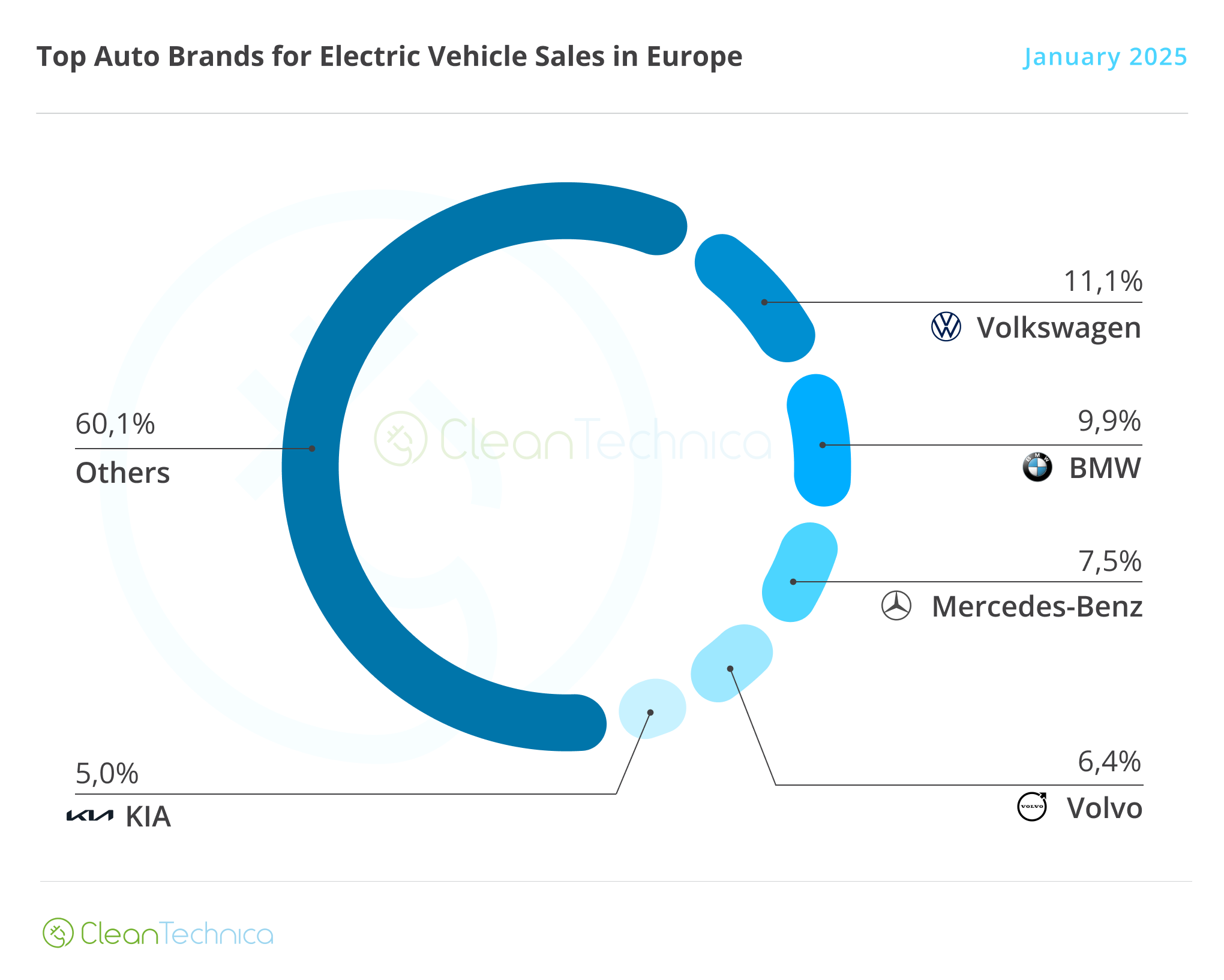

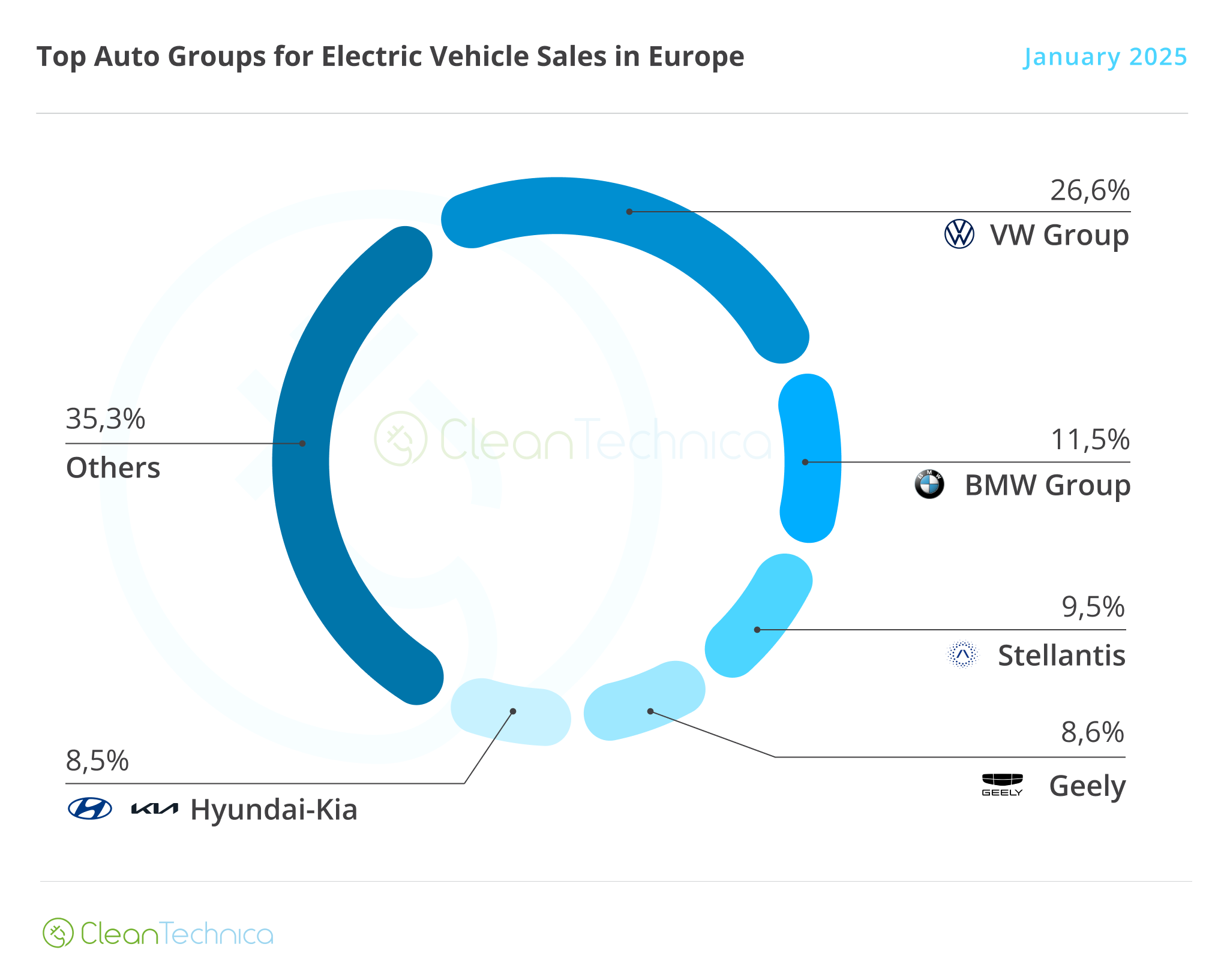

Brand and Manufacturer Rankings

In the brand rankings, MG was the biggest winner, growing 36% YoY to almost 23,000 units. Cupra also performed well, jumping 57% YoY, largely due to the launch of the Tavascan crossover.

![]

Tesla’s deliveries fell by 45% YoY, placing the brand at the 26th position overall. This decline stands counter to the narrative of consistent growth. It could indicate that Tesla has reached its demand thresholds, and that the question now is whether it will stabilize at the current levels or face further declines in the future.

In the manufacturer rankings, Volkswagen took the leadership position with an 11.1% share in January 2025. BMW followed with 9.9% and Mercedes with 7.5%. Kia, having a successful run with the new EV3, also made it into the top five.

Volkswagen Group leads in OEM rankings with a 26.6% market share, significantly higher than the 20.5% of a year ago. BMW Group came in second at 11.5%, with Stellantis in third at 9.5%.