January 2025: A Pivotal Month for the Global EV Market

Plugin vehicle registrations saw an impressive 18% year-over-year (YoY) increase in January 2025, exceeding 1.2 million units worldwide. Battery electric vehicles (BEVs) spearheaded this growth, rising by 24% YoY, while plug-in hybrid electric vehicles (PHEVs) experienced a more moderate 8% increase. This surge propelled plugin vehicles to a 19% share of the global auto market, with BEVs capturing 12%.

Several markets outside the usual spotlight contributed significantly to this global expansion. Analyzing markets with over 1,000 registrations in January, a strong showing of 100%-plus growth rates was observed, particularly in Asia. Malaysia, the Philippines, and Vietnam led the charge, while Denmark, Chile, Colombia, Turkiye, Saudi Arabia, and the UAE also demonstrated notable growth.

Vietnam’s EV Revolution

Vietnam stands out as a particularly compelling success story, largely due to the rapid expansion of the local brand, Vinfast. EV sales in the country skyrocketed by 311% YoY, reaching over 11,000 units in January.

Turkiye’s Dual Surge

Turkiye presents an even more unique case. The local brand Togg is experiencing rapid growth, and BYD is also witnessing exponential expansion. This has pushed the local EV market share above 10%, compelling established OEMs to adapt to stay competitive in a market of 1.2 million units per year. In January, Turkiye’s EV market registered more than 8,000 EVs, reflecting a 129% growth rate.

Global Market Outlook

With ongoing price wars in various markets and the introduction of new, more affordable models, the global EV market is anticipated to maintain a robust growth trajectory. Market analysts predict that the year could close with an EV market share exceeding 25% (with a 17% BEV market share). In the previous month, BEVs grew to over 816,000 units, increasing the BEV share within plugins to 65%, a 4-percentage point increase compared to the previous year.

China’s Influence and Model Performance

The Chinese market continues to exert considerable influence globally, representing 59% of global electric car sales in January.

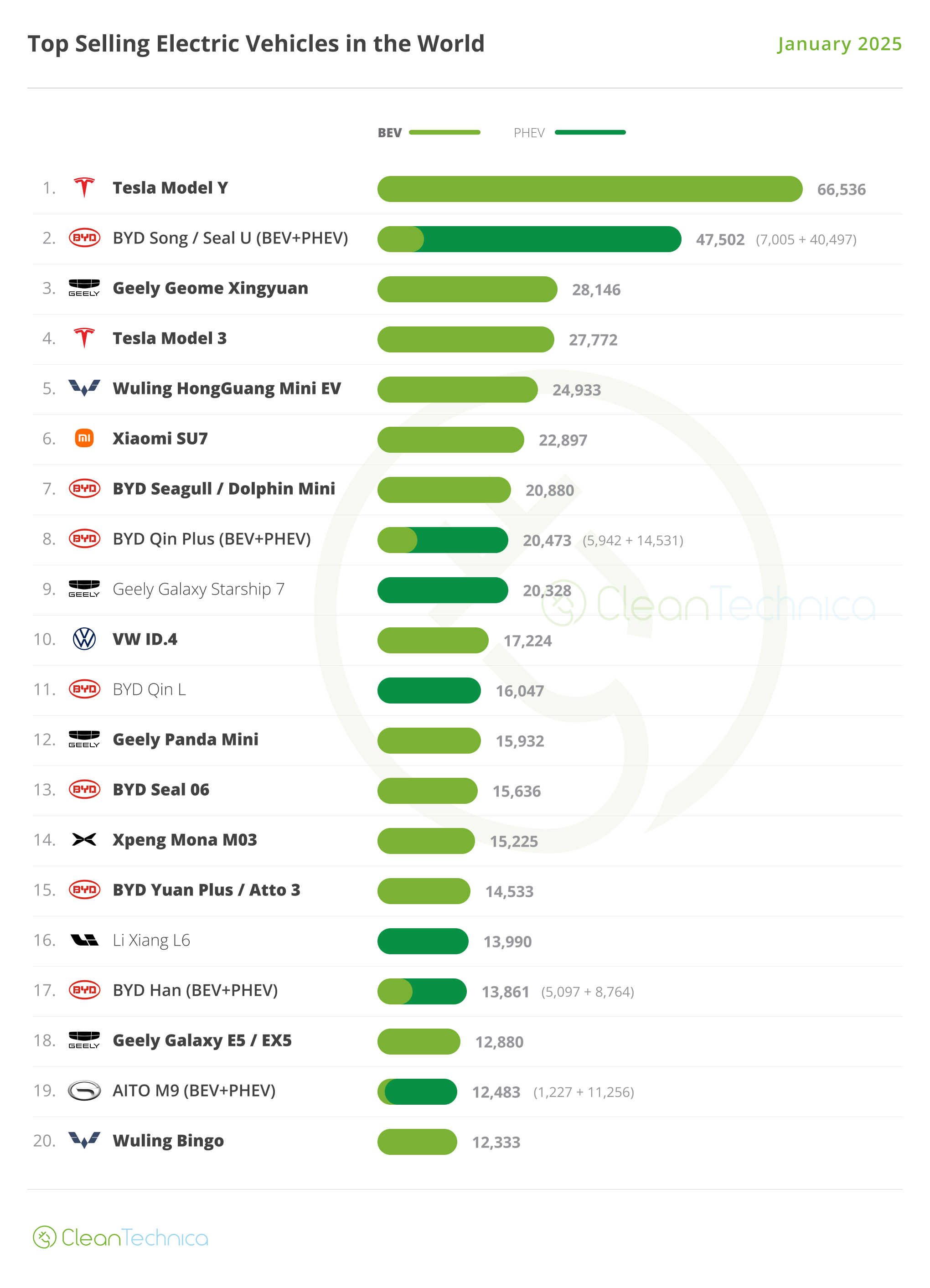

Examining top-selling models reveals interesting shifts. The Tesla Model Y, despite the usual top position, experienced a 6% sales decline to 66,536 units, marking its lowest performance since January 2023. The BYD Song maintained its runner-up position, mirroring its performance from the previous year.

Geely’s Ascent & Tesla’s Setback

A surprise emerged with the new Geely Geome Xingyuan surpassing the Tesla Model 3 for the third spot, recording 28,146 registrations. This marked the first time since 2022 that the Model 3 failed to secure a podium position, with deliveries down 10% YoY to under 28,000 units. The continued performance of the Model 3 and the impact of the Model Y refresh are closely watched.

Other Notable Models

Outside of the top three, the Wuling Mini EV, a compact four-seater, started the year in 5th place, trailing the US-based car by fewer than 3,000 units. In 6th place was the Xiaomi SU7 with nearly 23,000 units sold, despite a waiting list of 6-8 months. The Galaxy Starship 7, designed to compete directly with BYD’s Song, ended January in 9th place, recording 20,328 registrations.

The Volkswagen ID.4 achieved its best result since December 2023, securing over 17,000 registrations thanks to robust sales in Europe and the USA. Geely’s Panda Mini secured 12th position with 15,932 registrations, while the Galaxy E5 (EX5 in export markets) ranked 18th with 12,880 registrations.

Manufacturer Rankings: BYD Takes the Lead

BYD secured the top manufacturer position in January, with 278,000 registrations, more than twice the sales of runner-up Tesla (101,000 registrations). Tesla’s performance was the weakest in the last two years. The US brand’s dependence on its domestic market has increased; 49% of sales were in the USA, 33% in China, and 18% in the rest of the world.

Tesla’s Global Challenges

Tesla’s sales declined significantly in the rest of the world, even as the plugin market share grew by 24%. This raises questions about Tesla’s strategies in the face of increasing global competition.

Geely’s Rise

Geely emerged as the primary surprise in January, climbing to third place with nearly 93,000 registrations. This record achievement was driven by the expansion of the Geome (Xingyuan) and Galaxy (E5, Starship 7, and L7) lineups, combined with consistent sales of the Panda Mini EV.

Other Significant Players

Xpeng jumped to 7th place, surpassing Li Auto as the highest-selling startup. Another rising brand is Toyota, which experienced strong sales of its BZ4X SUV and PHEV lineup, potentially stabilizing its place in the top 10 rankings.

Ford ranked 19th thanks to a growing lineup, with Lynk & Co joining the table at 20th due to the success of its 08 midsize SUV. Within the OEM rankings, BYD leads again (23.6%), followed by a surging Geely (11.8%) that has surpassed Tesla (8%). Comparing performance, Geely’s rise is contrasted by Tesla’s decline over the past two years. This highlights the need for Tesla to provide more variety of choices for consumers which BYD and Geely clearly do.

BEV Rankings

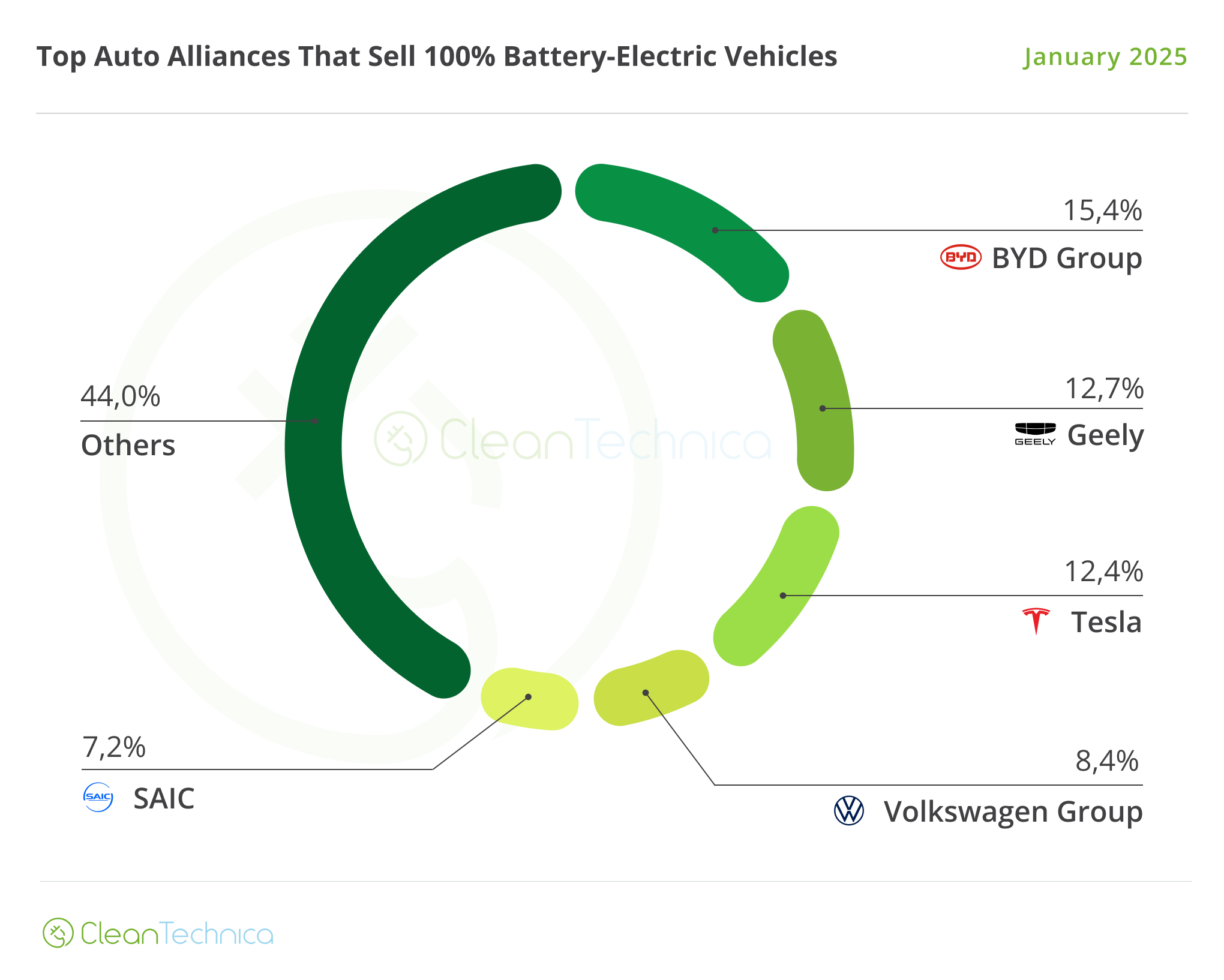

Looking at BEVs specifically, there were 816,427 registrations in January, representing 65% of plugin sales. A major shift occurred at the top, where Tesla dropped to third place with a 12.4% share, down from 17.6% a year earlier. BYD took the lead (15.4% share), followed by Geely (12.7%).

In the BEV segment, Tesla is expected to attempt a recovery in March. Whether Tesla can return to the leadership position remains a key point of interest.

The Road Ahead

The January 2025 EV market figures underscore the dynamic nature of the global EV landscape. BYD’s strong performance and Geely’s impressive growth signify a changing of the guard, while Tesla faces the pressure of intensifying competition. The coming months will be critical in determining the long-term trends and power dynamics within the EV market.